Magyar Telekom, Hungary’s leading telecommunications group, reported much better figures for the third quarter of 2017 than analysts expected. Yet, for some reason, management have turned pessimistic by the end of the year and have not changed the conservative full-year objectives, although fundamental processes turned out rather well and IT projects co-financed by the European Union also help shore up MTel’s numbers.

The key messages are:

Jump in total revenues and profit.

MTel is a great winner of the EU’s IT projects, which is a key driver of revenues.

Indebtedness drops, remains well within the management’s comfort zone.

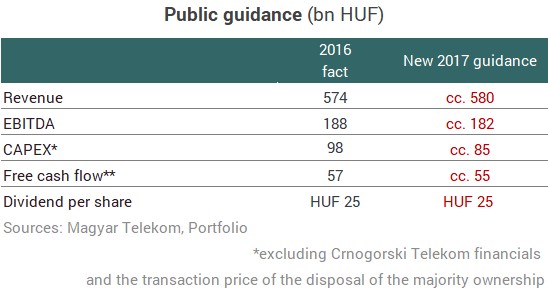

Management do not alter guidance for this year, partly because it expects strong competition.

Dividend per share target remains HUF 25, although the expected free cash flow would give the company room for a much greater dividend.

Pretty, pretty

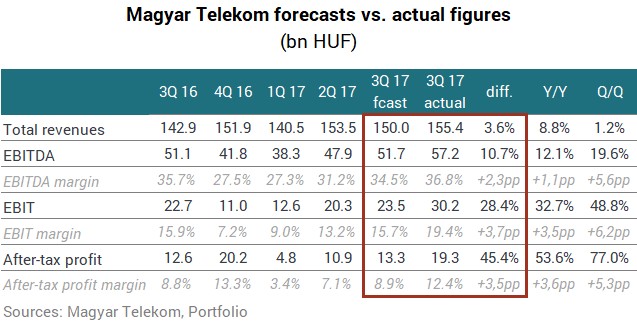

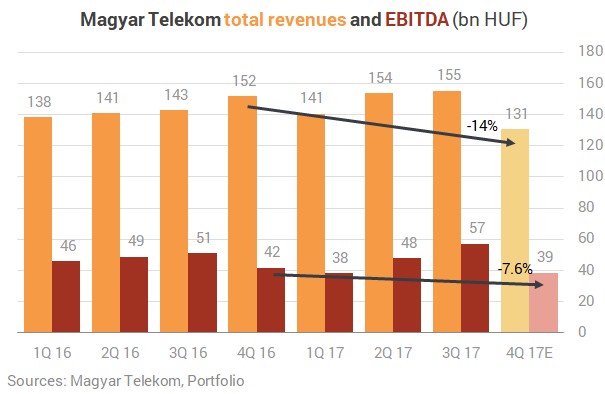

MTel published robust Q3 figures today. Its revenues rose 8.8% yr/yr to HUF 155.4 billion, EBITDA went up 12.1% to HUF 57.2 bn, and after-tax profit leaped 53.6% to HUF 19.3 bn. Total revenues came in 3.6% higher than the market consensus, whereas EBITDA and after-tax profit beat the market’s call by 10.7% and 45.4%, respectively.

Magyar Telekom had a great run

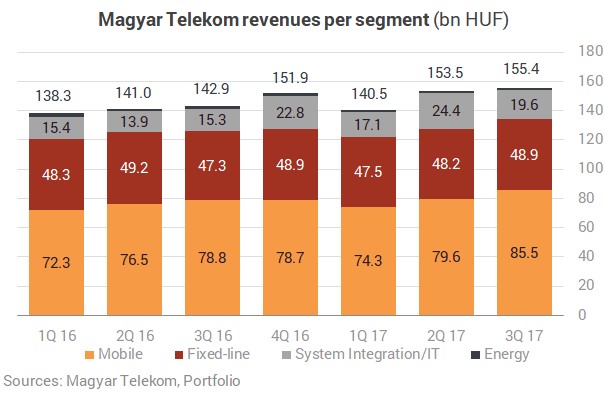

MTel’s consolidated revenues have never risen as much as in Q2 (8.9%) and Q3 (8.8%) as far as we can remember. Well, it’s not exactly easy to make comparisons here since due to the sale of the group’s Montenegrin unit, we have comparative figures only since the start of 2016. According to long data series, though, we should go back well before the crisis to find similar growth rates. The jump in Q3 revenues stems from the great performance of two areas:

Growth in mobile revenues (+HUF 6.7 bn, +8.5% yr/yr) were driven by sustained increase in mobile service revenues resulting from strong mobile data demand, coupled with increasing visitor data usage (reflecting the EU Roam Like Home legislation that came into force in mid-June this year), and equipment sales. The latter was also supported by the provision reversal relating to the ceased loyalty programme.

System Integration and IT (SI/IT) revenue increase (+HUF 4.3 bn, +28.4%) reflects high demand for equipment deliveries particularly in the Hungarian public segment. The increase was primarily driven by the acceleration of EU fund inflows into Hungary, boosting levels of high volume software and hardware delivery projects.

Fixed line revenues increased by 3.3% year-on-year to HUF 48.9 billion in Q3 2017 due to positive trends in broadband, TV, data and equipment revenues coupled with some slowdown in the decline of voice retail revenues.

Energy services revenues decreased by 7.7% yr/yr in Q3, due to a smaller electricity customer base and expiry of the few remaining universal gas contracts. This segment contributes less than 1% of group revenues, since MTel delivers electricity only to over 89,000 customers vs. a peak of over 109,000.

After the divestment of its operation in Montenegro, MTel has a subsidiary only in Macedonia where revenues contracted 3.3% yr/yr in July-September, while mobile revenues were stable and fixed-line revenues fell 4.8% and customers were lost both in the fixed-line and mobile segments.

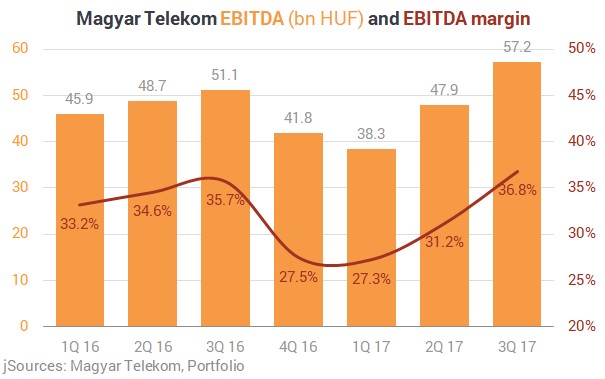

EBITDA was 12.1% higher year-on-year at HUF 57.2 billion in Q3 from increased revenue, one-off income from real estate sales and cost optimisation measures (although operating expenses still climbed 5.5%). In Montenegro, a temporary postponement of marketing activities helped MTel boost EBITDA by 4.5%. EBITDA marin edged up to 36.8% from 35.7%, which is an outstanding figure. We need to go back five years to find a higher reading.

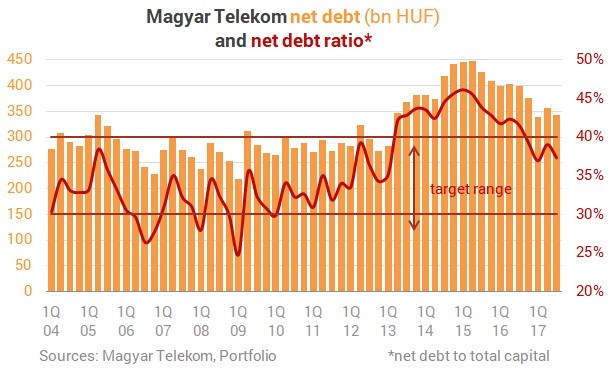

Free cash flow from continuing operation (FCF) overall decreased by 29% yr/yr to HUF 27.4 billion in January-September. The reduction reflects a deterioration in receivable balances as well as one-off gains (from the sale of Origo and Infopark Building G) of HUF 11.3 billion which supported 9M 2016 results. The FCF guidance was left on hold at cc. HUF 55 bn, which would allow higher dividend than the targeted HUF 25 per share. Indebtedness would not tie the hands of the management, either, because the net debt dropped HUF 13.7 bn to HUF 343.7 bn and the net debt ratio came in at 37.4%, well within the management’s comfort zone.

[...] whilst we expect the various initiatives we have introduced in both the mobile and fixed line segments to continue to support our performance, we also anticipate an increase in competitive pressures both in Hungary and Macedonia. As such, our public targets for the full year 2017 remain unchanged

, commented CEO Christopher Mattheisen.

If we deduct the Q1-Q3 profit from the full-year guidance, we’ll find that management are rather pessimistic: In the fourth quarter, revenues should drop 14% yr/yr to HUF 131 bn and EBITDA should be down by nearly 8% at HUF 39 bn, according to the current estimates. This is hard to take seriously, especially because Q4 tends to be the best quarter of all at the group. So, something (SI/IT?) should really go awry by year-end if the targets are to be met.

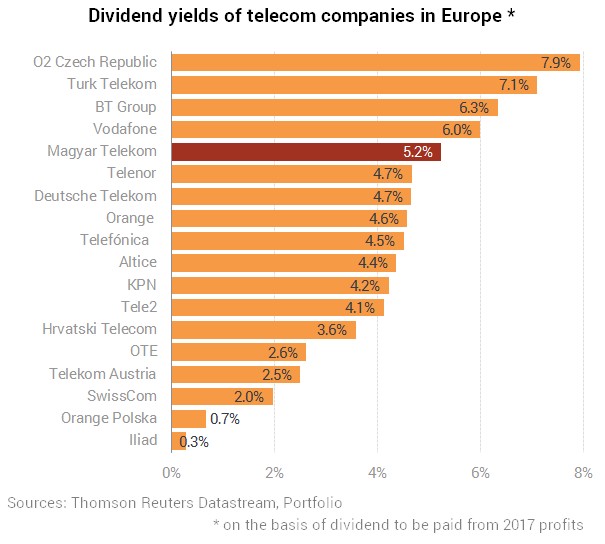

Although on the basis of its free cash flow, MTel would be able to pay much more than HUF 25 DPS, the 5% plus dividend yield is not bad at all in European comparison.

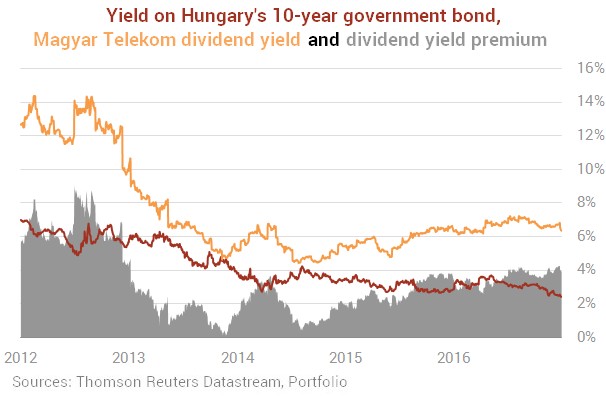

Analysts continue to project a rise in dividend and that would give us a dividend yield of around 6%. At that level, Telekom shares would offer quite a handsome premium over the yield of Hungary’s government bonds at the long end of the curve.

Charting is displayed using TradingView's technology, a platform, where you can build advanced charts,

spot upcoming trends in the stock screener, and find inspiration in multiple trading ideas