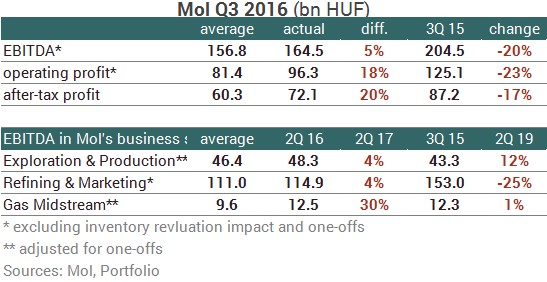

Hungarian oil and gas group Mol reported strong figures for the third quarter of 2016, but the results were overall weaker than in previous peak quarters. The group’s key profits were above analysts’ consensus estimates. In view of the January-September results, Mol’s management raised their full-year profit target.

for the first time since 2011, Exploration & Production reported yr/yr EBITDA growth on the back of higher volumes and declining costs;

worsened performance in Refining & Marketing, with petrochemical and refining margins down;

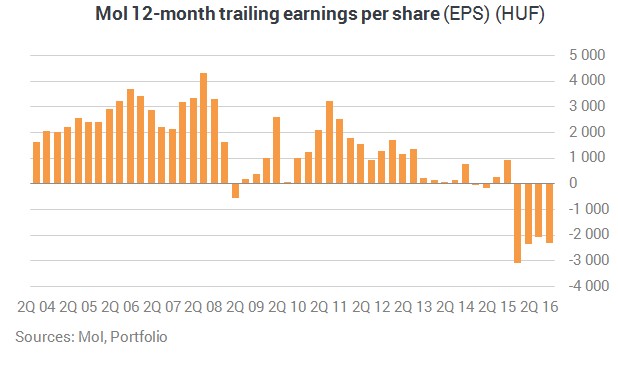

decreased 12-month trailing earnings per share (EPS);

annual average EPS forecast has already been exceeded;

CAPEX dipped by 34%

indebtedness indicators remain stable

How was the third quarter?.

As it was already expected in view of the external sectoral environment, Mol’s key profits dropped significantly in annual terms in the third quarter. Clean CCS EBITDA came in 20% lower than in the base period. However, analysts’ profit expectations were overshot. Downstream beat the average estimate by 4% and Mol’s consolidated after-tax profit came in 20% higher than expected.

What have affected the results?

The key factors affecting Mol’s different segments in the first quarter were the following.

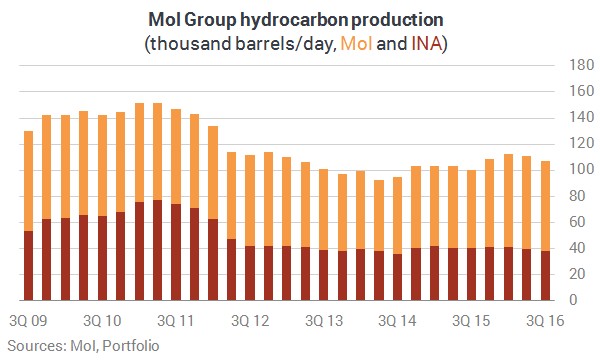

Upstream (Exploration & Production)

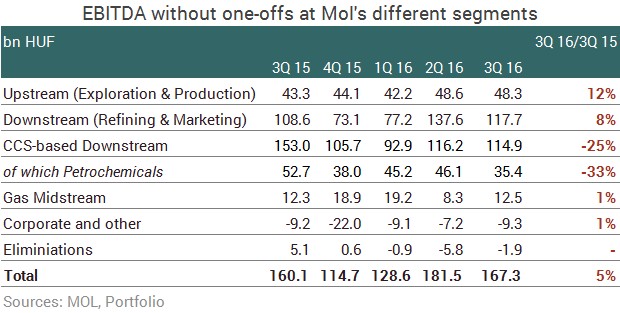

The segment’s EBITDA adjusted for one-offs grew by 12% year on year, which is the first growth in annual terms recorded here since 2011. This was the result of the following factors:

the average price of Brent-type crude declined 9% compared to the base period;

as a consequence, realised hydrocarbon prices also fell; Mol recorded a 4% decline at crude prices and 24% fall in gas prices therefore the average realised hydrocarbon price went down 14%.

The unfavourable impact of this was compensated by the fact that

Mol’s production volume grew by 6% yr/yr

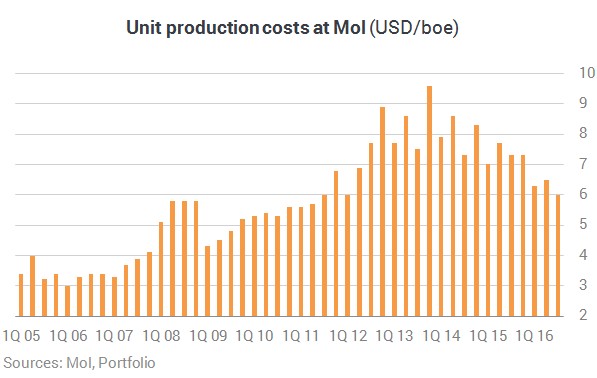

and unit cost of production dropped 17% to USD 6 per barrel, the lowest figure we have seen since Q1 2012.

80% of the improvement stemmed from actual Opex reduction, as the currency impact was negligible

The new Upstream Programme is already yielding results, as we can see. Mol’s unit Opex target is 6-7 USD /boe, which compares with 6.3 in Q3. Organic Capex declined by 33% in the third quarter, and exploration capex dipped by more than 70%. This is not a unique phenomenon, though, as in the altered oil price environment other large oil companies have similar processes. Mol’s 2016 target is cc. 15-30% organic Capex decrease.

Mol’s strategy in Upstream remains unchanged: the company wants to have assets that create value and are self-financing even at USD 45-50 oil price. Mol achieved free cash flow of USD 140 million at an average of USD 42/bbl Brent price in Q1-Q3. Management set their target at a positive cash flow for this year.

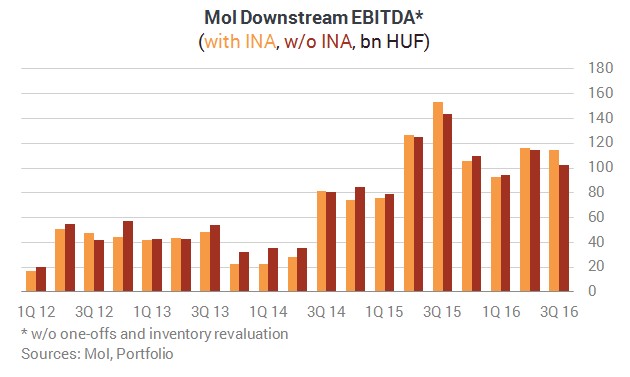

Downstream (Refining & Marketing)

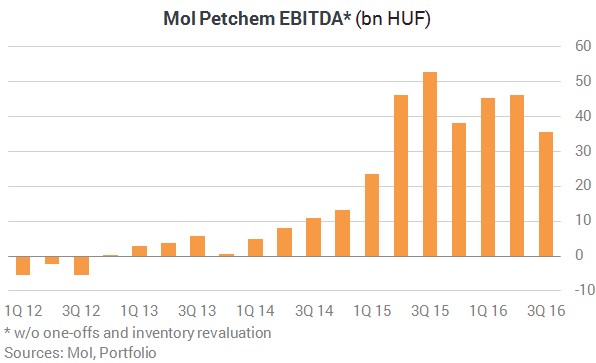

Downstream Clean CCS EBITDA declined 25% over a strong base. The segment includes three main activities: crude processing and trade, retail sales and petrcochemicals. The segment was hit by refining and petchem margin normalisation and the planned maintenance, which was only partly offset by strong retail EBITDA.

Petchem The segments Clean CCS EBITDA dropped 33% to HUF 35 bn due to the following factors:

petchem production decreased 3% and petchem sales fell 9%;

Integrated petrochemical margin dipped by 21%

Retail sales Clean CCS EBITDA in the segment rose 24% yr/yr. Retail sales grew by 10%, as a result of larger consumption relating to lower prices and the increase in the number of petrol stations. Mol added 122 units (+17%) to its network of pumps compared to the base period, which already includes the Hungarian and Slovenian petrol stations acquired from Italy’s Eni. Mol has been expanding on the region’s retail markets rather actively for years.

Gas Midstream

Natural gas transmission showed steady results on an annual basis, both in Q3 and January-September. Lower capacity fee revenues (yr/yr) caused by regulatory changes were offset by a strong transmission volume growth.

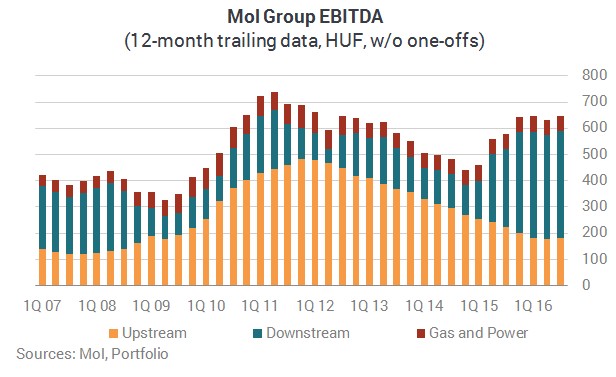

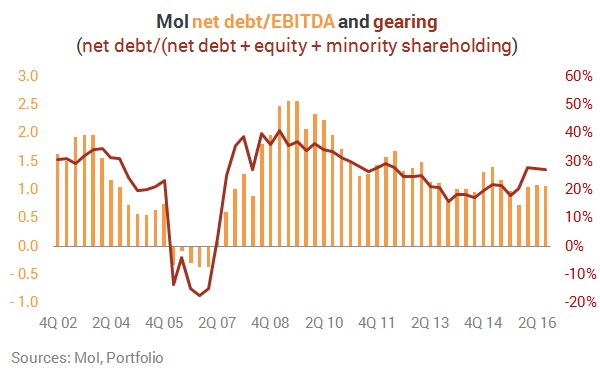

Group figures, gearing

As a result of the above, Mol posted HUF 164.5 billion Clean CCS EBITDA in the third quarter, 20% less than a year earlier;

Operating cash flow dropped 22%;

The 12-month trailing EPS dropped, but it still includes a massive, write-off related loss incurred in Q415, which will be out of the picture next quarter.

The January-September EPS is 22% over the full-year EPS estimate;

Group level Capex plummeted 34% yr/yr, whereas organic Capex declined by 22%;

Gearing metrics remained stable, well within Mol’s comfort zone (net debt/EBITDA should be under 2% this year).

Management comment, plans

Chairman-CEO Zsolt Hernádi commented on the results:

“MOL continued to deliver strong results and cash flows in Q3 2016 helped by its resilient integrated business model and relentless focus on efficiency and cost discipline. We are now confident that we can even outperform our initial plans for the year, hence we upgrade our 2016 Clean CCS EBITDA guidance to around USD 2.2bn.

“We also look forward to unveiling more details regarding our strategic plans and targets next week at our Capital Markets Day. We believe that our high quality, efficient asset base and resilient integrated business model, which have been tested by extreme macro conditions and proved to be capable of consistently generating strong free cash flows over the years, serve as an excellent base for the implementation of our new long-term strategy (“MOL Group 2030 - Enter Tomorrow"), which the Board of Directors approved in October."

On the back of a strong first nine months delivery (USD 1.68bn), Mol upgraded its Clean CCS EBITDA target to around USD 2.2 bn for 2016 (of which USD 1.68 bn have been reached). The previous guidance was around USD 2.0 bn.

As for Mol’s free cash flow generation, the company has targeted positive cash flow for this year. The group has made great progress in this respect, as well, as its free cash flow was up at nearly USD 1 bn by the end of September.

Charting is displayed using TradingView's technology, a platform, where you can build advanced charts,

spot upcoming trends in the stock screener, and find inspiration in multiple trading ideas